Grain Market Overview March 23

March 23, 2016Grain Market Overview March 30

March 30, 2016Commodity Market News March 28

Summary

The Grain complex has managed to continue trading sideways to slightly up but that could all change when the USDA releases its quarterly Grain Stocks report this Thursday, March 31st. This upcoming report historically sets the market tone for a few months to come. The Ag markets were closed on Friday and the trading volume was pretty light last week ahead of the long Easter holiday weekend. The shortened week was uneventful with hardly any market moving information making its way across the newswire.

Just over a week ago it appeared that hedge funds threw in the towel on short positions in agricultural commodities at one of the fastest paces on record, in many cases realizing losses –Managed money, a proxy for speculators, turned from a net short position in the main US traded Ags of 213,000 contracts (the 2nd largest in history) to a net long of some 34,000 lots in the week of March 16th, according to data from the Commodity Futures Trading Commission (CFTC). This swing in positioning of 247,000 lots was the 3rd largest on records going back to 2006. Overall investors have not been as bearish towards commodities making short traders skittish. Additionally, some Ags have gained strength from a rebounding Brazilian Real, which boosts the dollar value of commodities such as coffee and sugar in which Brazil is particularly important.

Corn

May Corn futures posted its tightest weekly trading range since mid-December. May Corn gained 3 cents on the week and December Corn rose 1 3/4 cents. Both had inside range bars on their weekly charts failing to eclipse the previous week’s high or low. This perceived indecision could very well persist this week ahead of the USDA Quarterly report.

After stringing together 4 weeks of strong export sales numbers Corn came in below trade estimates last week. Estimates ranged from 900k to 1.1M MT with the actual coming in at 803.2k MT. The total commitments were at 74% of the USDA export total.

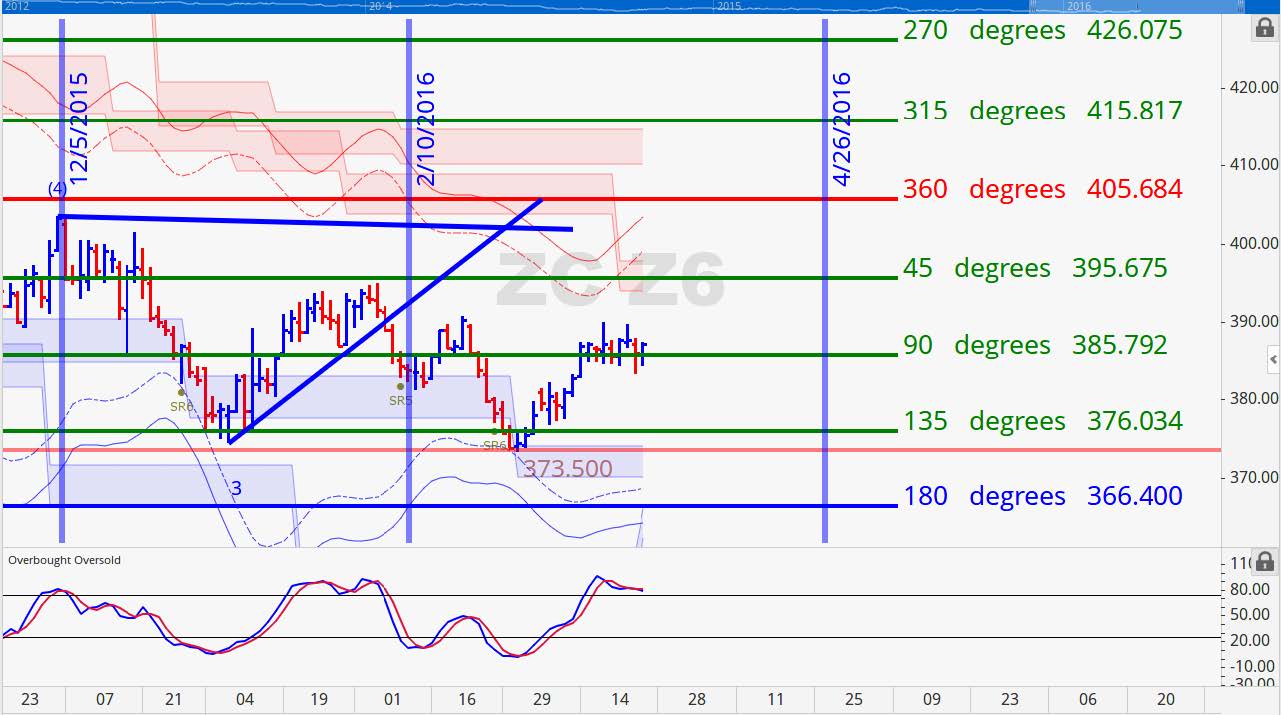

Last week May Corn futures were not able to separate from the 366 price level. The 90 degree mark of 366 1/2 has been support since March 14th. If any buying enters the market and is able to close above 373 (a point of control derivative) the first area of resistance/price objective would be volatility based resistance at 377 1/2 to 381 1/2. The point of control rests at 396. So, in our estimations it will be challenging for the price to get much higher than 400.

The 90 degree mark for the December contract has been 385 3/4 which has been functioning as a price node in the middle of the price action for the last two weeks. A break of either 383 or 391 looks to send prices to either 374 or 394. It is looking like somewhere between March 31st and April 7th could be the demarcation point that triggers a potential decline through late May.

May 2016 Corn Charts

Soybeans

The supply and demand narrative for the Soybean market continues to be bearish but there remains a political factor that could play a role in changing the price action. Observers are acknowledging the possibility of a new Brazilian president by the time the summer Olympics roll around. The implied risk is the potential for a disruption in Brazil’s ability to export its huge Soybean inventory. There is not any indication of disruption as of yet but there is an additional perspective that must be considered when crafting your marketing program.

Last week, Soybean export sales were at the low end of trade estimates coming in at 410.8k MT. Estimates ranged from 400k to 600k MT. Total commitments were at 95% of the USDA export total. May and November Beans rose 13 cents last week.

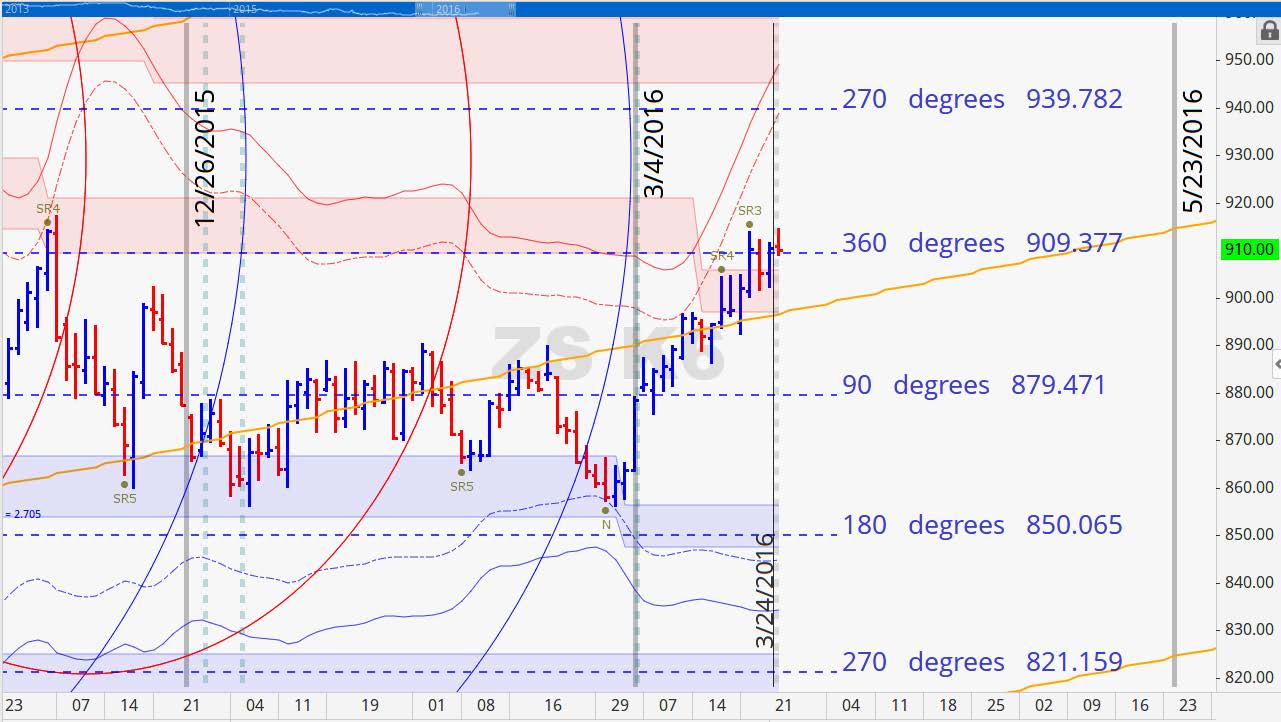

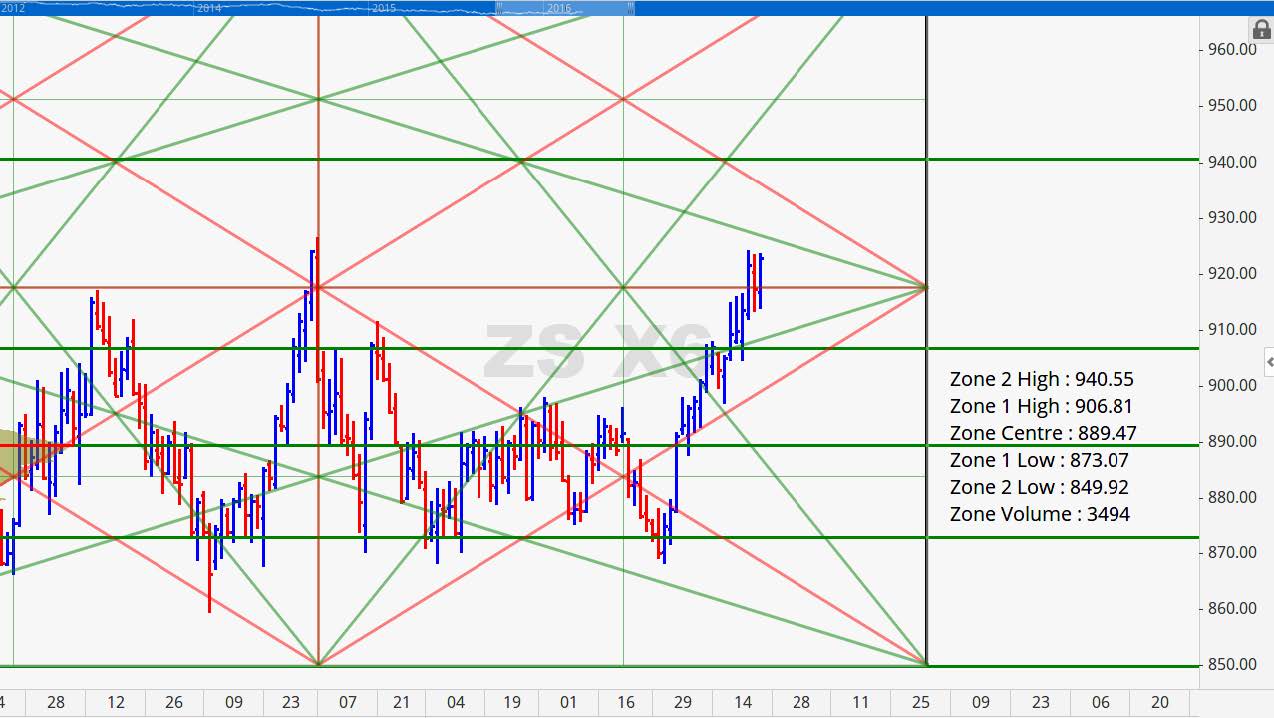

Our potential cycle turn date of March 24th occurred on the eve of Good Friday. The May Soybean contract has moved up into this date. A couple trading days either side of that cycle point would still qualify as a turn so we have our attention on alert with prices at a key 360 degree level of 909 1/2. The high last week was 914 and the low as 892 1/4. If we are able to break 892 prior to breaking 915 this week we believe that Beans could be in for a move down into mid to early May with a potential to reach the 825 to 820 area. The current point of control rests at 903 1/2. Outside of some mitigating factors the narrative remains bearish but the political environment could make for a surprise.

May 2016 Soybean Charts

Wheat

Cold temperatures hit SW Kansas over the weekend coming in even colder than expected. Damage assessment is not finalized yet so the magnitude of damage is unclear for now. Crop conditions indicated that only 20% of the Kansas crop was jointing. Additionally, conditions showed that Kansas and Texas were both up 1% good/excellent, while Oklahoma dropped 4% from the previous week. Egypt received 6 offers for Wheat they tendered and ended up buying 60,000 tons of French Wheat. Sellers continue to be unwilling to participate with Egypt because of their lack of clarity around ergot regulations. The recent strength in the US Dollar has kept US Wheat uncompetitive right now.

July Wheat was up 1/2 cent last week and held up well on top of our 270 support level of 465 1/4. In fact it closed about the Fibonacci retracement level of 468 3/4 with a strong reversal close on Friday. It touched off of volatility based support on the 18th of March and looks to make a run to resistance at 487 once again. The way in which if responds to the 487 level should it reach there this week could be an indication that price might make a run to 500.

July 2016 Wheat Charts

Crude Oil

Futures were choppy last week. We rolled from the April contract to the May contact and the price action has moving down from being overbought. We still have April 8 as a potential time cycle for a turn and it appears that prices want to move down into that timeline give the current daily price action. Our levels have been adjusted. Between 35.40 and 36.90 is potent support going into the early April timeline and overhead resistance is at 43.95. This contract posted several closes above 39.74 suggesting that a minimum price objective of 43.95 is probable.

Grain Market Overview October 11

Read more